GXO's North America Bet: How Reshoring and Tariff-Driven Demand Are Fueling 3PL Automation Growth

GXO Logistics just reported Q4 2025 results that beat Wall Street expectations — $3.5 billion in revenue, 87 cents adjusted EPS — and the message from CEO Patrick Kelleher was unmistakable: North America is the growth engine, and automation is the fuel.

The $250 Billion Opportunity

North America currently represents about a third of GXO's global business, but Kelleher sees that share growing substantially. In an interview with FreightWaves, he described the North American contract logistics market as a $250 billion addressable opportunity — and growing.

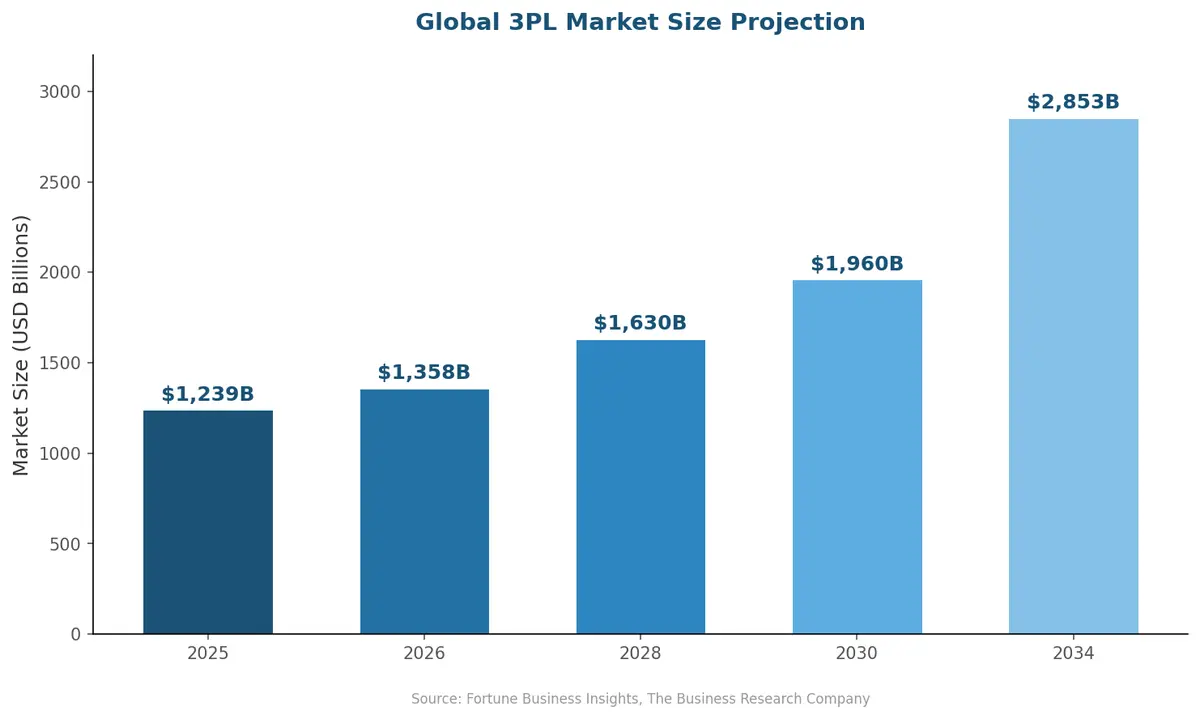

That growth isn't hypothetical. The global third-party logistics market hit $1.24 trillion in 2025 and is projected to reach $2.85 trillion by 2034, growing at roughly 10% CAGR.

North America is leading the charge, driven by reshoring momentum that shows no signs of slowing.

North America is leading the charge, driven by reshoring momentum that shows no signs of slowing.

According to the Reshoring Initiative, approximately 240,000 jobs were reshored to the United States in 2025 alone. Meanwhile, 58% of CEOs with overseas operations are now actively considering reshoring — up from historical averages that hovered around 30-40% just a few years ago.

Tariffs Are Reshaping Supply Chain Geography

The current tariff environment initially created decision paralysis. Kelleher acknowledged that customer decision-making "was paused almost as a result of some of the tariff decisions and the changing landscape around trade." But that pause is over.

What's emerged is a fundamental rethinking of supply chain geography. Companies aren't just adjusting sourcing — they're redesigning entire logistics networks. GXO operates 67 free trade zones and bonded facilities globally and is actively repositioning its North American footprint along key U.S.-Mexico trade corridors to capture nearshoring demand.

The verticals driving this shift tell the story: aerospace and defense, industrial technology, and life sciences — sectors where supply chain security and domestic production capacity have become strategic imperatives, not just cost optimization exercises.

For shippers navigating these changes, the complexity is staggering. New manufacturing locations mean new distribution patterns, new carrier relationships, new compliance requirements, and new visibility gaps that didn't exist when everything flowed from a handful of Asian ports.

Automation as the Margin Lever

Here's where the economics get interesting. GXO has deployed more than 20,000 robots across its global operations and is piloting humanoid robots in live warehouse environments, with a production-ready demonstration expected in California this year.

But the robot count is less important than the strategic logic behind it. Contract logistics has historically been a labor-intensive, thin-margin business. Automation changes that equation fundamentally. GXO expects roughly 20 basis points of margin expansion in 2026 — incremental, but compounding year after year as automation penetrates deeper into operations.

The company's centralized AI platform, GXO IQ, is rolling out across more than 1,200 operations globally to standardize tools, improve labor planning, and drive productivity. This isn't isolated automation in a few showcase facilities — it's systematic deployment at enterprise scale.

Kenco's 2026 Innovation Report reinforces this trend across the broader 3PL industry. Their survey of over 150 supply chain executives found that 83% have a dedicated 2026 innovation budget, with nearly half reporting budgets of at least $500,000. The top drivers? Inflation (45%), labor shortages (28%), and sustainability (27%). Automation isn't optional anymore — it's how 3PLs survive margin pressure.

What This Means for Shippers Choosing a 3PL

The reshoring-plus-automation trend creates a clear dividing line between 3PLs that are investing in technology and those that aren't. For shippers evaluating contract logistics partners, several factors now matter more than they did even two years ago:

Technology infrastructure depth. A 3PL's automation capability directly affects your cost per unit handled. Ask about robot density, AI-driven labor planning, and warehouse management system sophistication — not just square footage and geographic coverage.

Network flexibility for reshoring. As manufacturing footprints shift, your logistics network needs to shift with them. Providers with presence along emerging trade corridors (particularly U.S.-Mexico) and free trade zone expertise will deliver measurable advantages.

Data integration capability. GXO's investment in a unified AI platform reflects a broader truth: 3PLs that can't integrate seamlessly with your TMS, ERP, and order management systems create coordination gaps that erode the efficiency gains automation delivers.

Scalability without capital risk. The outsourced model thrives in volatility. As Kelleher put it: "When customers change, we play a big role in helping our customers thinking through and making those changes." The right 3PL absorbs the capital risk of automation investment while passing through productivity gains.

The Bigger Picture

GXO's North America bet reflects a structural shift in how global supply chains operate. The era of optimizing purely for lowest unit cost from a single offshore source is giving way to a more complex calculus: resilience, speed, compliance, and total landed cost including tariff exposure.

This creates both opportunity and complexity. Companies that invested early in digital logistics infrastructure — integrated TMS platforms, real-time visibility, automated carrier management — are positioned to capitalize on reshoring without drowning in operational complexity.

Those still managing logistics through spreadsheets and phone calls face a widening gap that gets harder to close with every quarter.

Navigating reshoring complexity and 3PL selection? Contact CXTMS for a demo of how our platform helps shippers manage multi-node logistics networks with real-time visibility and automated coordination.