Supply Chain Digitization Becomes Infrastructure: What Q4 2025 Earnings Reveal About 2026 Tech Spending

Something shifted in earnings season this quarter. When executives from FedEx, Caterpillar, Dollar General, and Ahold Delhaize addressed investors about their 2025 capital expenditures and 2026 roadmaps, supply chain technology wasn't filed under "IT improvements." It was presented as durable infrastructure — on par with new facilities, fleet upgrades, and network expansion.

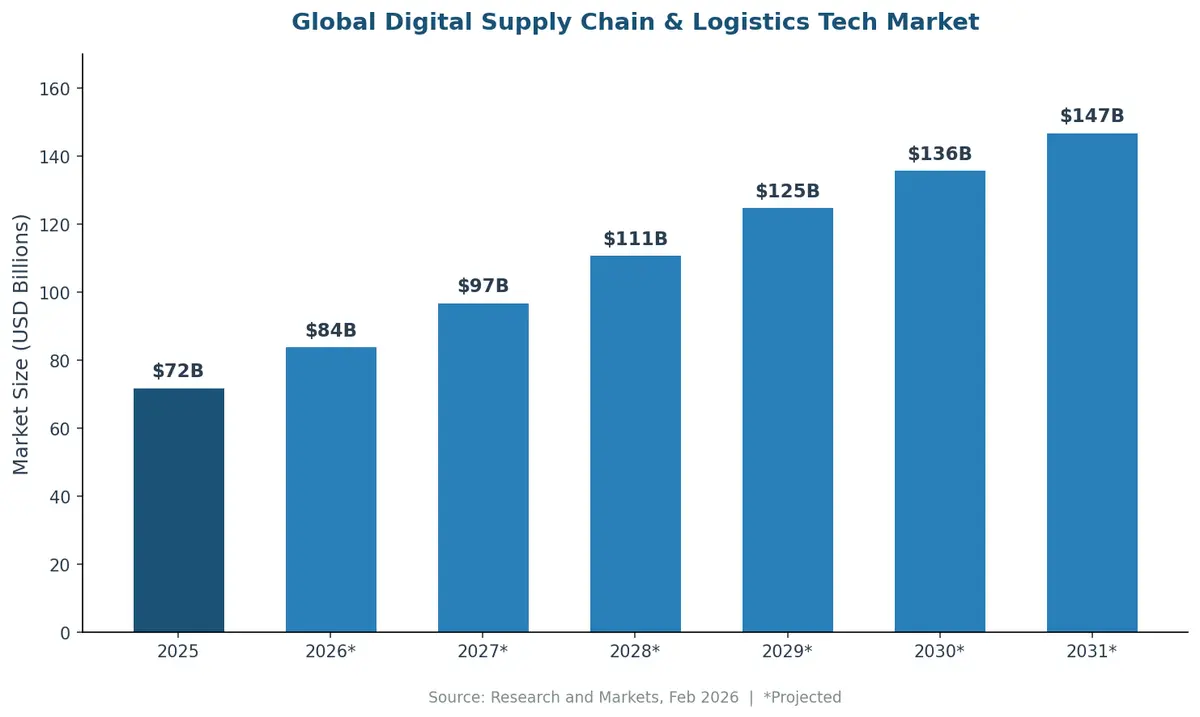

That rhetorical shift carries real dollars behind it. The global digital supply chain and logistics technology market hit $72 billion in 2025 and is projected to reach $146.92 billion by 2031, according to a February 2026 research report. That's not incremental growth — it's a doubling in six years, signaling that companies across every vertical now treat logistics digitization as a non-negotiable investment.

From Cost Center to Capital Infrastructure

For most of the past decade, supply chain technology lived in the productivity improvement bucket. Companies bought tracking systems, warehouse automation, or predictive analytics to squeeze out costs or shorten cycle times. The business case was built on savings.

That framing has expired. As PYMNTS reported from Q4 earnings analysis, three themes dominated investor calls this quarter:

- Capex is shifting upstream. Companies are investing in supplier integration, orchestration layers, and data capture systems — not just warehouse floors.

- AI investment is inseparable from supply chain redesign. The physical backbone required for AI-driven commerce is being built now, and logistics sits at its center.

- Competitive advantage has migrated to execution certainty. Firms that can promise delivery timelines, inventory accuracy, and responsiveness are winning contracts in volatile markets.

The implication is clear: supply chain technology is no longer something you optimize after scaling. It's a prerequisite to scaling at all.

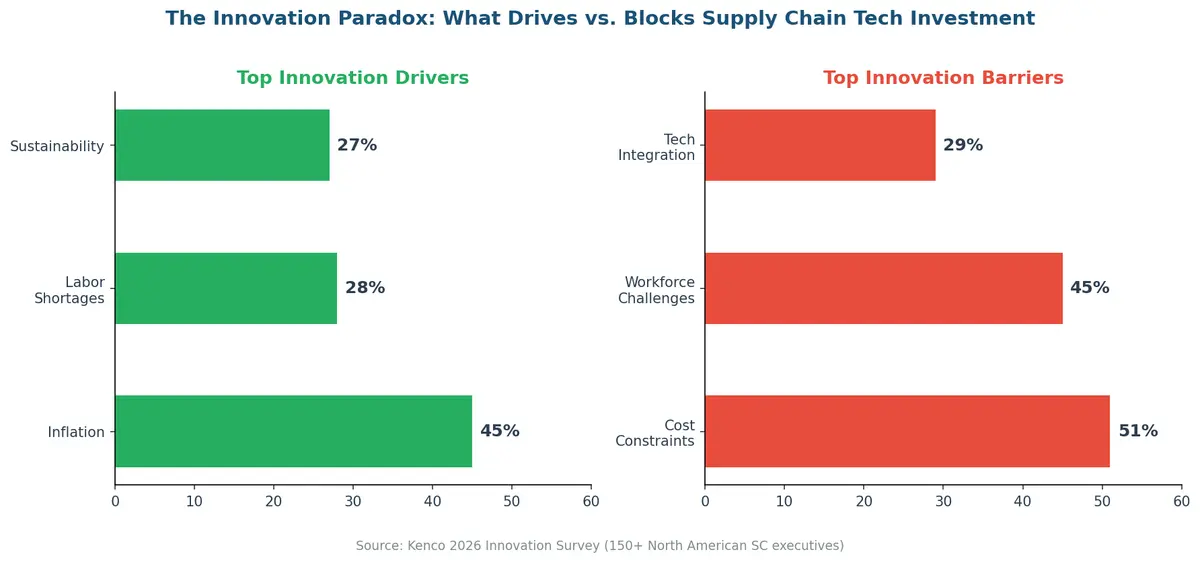

The Innovation Paradox: Inflation Drives Urgency While Constraining Budgets

Kenco's 2026 Innovation Survey Report, surveying over 150 North American supply chain executives, reveals a paradox at the heart of current investment decisions. Organizations increasingly depend on innovation to mitigate inflation — yet inflation itself makes those projects harder to fund.

The numbers tell the story:

- 45% of respondents cite inflation as their primary innovation driver, followed by labor shortages (28%) and sustainability priorities (27%).

- Cost constraints (51%), workforce challenges (45%), and technology integration issues (29%) remain the biggest barriers to progress.

- Despite these headwinds, 83% of respondents reported having a dedicated 2026 innovation budget.

- Nearly half of companies (49%) have innovation budgets of at least $500,000.

What's notable is where the money is going. Executives are prioritizing foundational improvements — quality (33%), inventory management (27%), and labor efficiency (23%) — over flashy emerging tech. A full 42% favor established technologies, and 43% prefer blending existing and emerging solutions. Reliability is outweighing novelty.

The CFO's New Calculus

The shift from "IT project" to "infrastructure" changes who controls the budget and how ROI is measured. When supply chain tech was a cost-optimization play, it lived under the CIO's discretionary spending. Now it sits alongside fleet replacement and facility expansion in the CFO's capital plan.

This reframing has several practical consequences:

Longer investment horizons. Infrastructure spending isn't evaluated on 12-month payback periods. Companies are making 3-to-5-year commitments to platform architectures, knowing that the compounding benefits of integrated data, automation, and orchestration take time to materialize.

Vendor consolidation pressure. The Kenco survey found that organizational challenges — not technology — create the biggest implementation hurdles. Misalignment across Operations, IT, HR, Risk, and Legal delays projects more than any technical limitation. This is driving companies toward unified platforms that reduce integration complexity rather than adding yet another point solution.

3PL expectations are rising. Companies increasingly depend on their logistics partners for strategic guidance, not just warehouse space. Kenco reports that 37% of respondents expect their 3PL to provide support across strategy, implementation, funding, and ongoing operations — turning contract logistics into a technology partnership.

What the $72B-to-$147B Trajectory Means for Mid-Market Shippers

The market doubling isn't being driven equally across all segments. North America accounts for over 80% of global digital supply chain spending, with the U.S. market anchoring that dominance. But the spending concentration among enterprise players creates both risk and opportunity for mid-market shippers.

The risk: As large retailers and manufacturers invest heavily in orchestration platforms, real-time visibility, and AI-driven demand forecasting, they raise the performance bar for everyone in their supply chain. Suppliers who can't match that digital capability get left behind — or charged penalties for non-compliance.

The opportunity: The same technology that enterprise players are deploying at scale is becoming accessible to mid-market companies through cloud-native TMS platforms. You no longer need a $10 million implementation budget to get real-time tracking, automated carrier selection, or exception-based workflow management.

The key difference between companies that successfully navigate this transition and those that don't often comes down to platform architecture. Companies running fragmented point solutions — one tool for rating, another for tracking, another for document management — face the exact organizational misalignment problems that the Kenco survey identified as the primary barrier to innovation.

Digitization Is No Longer Optional

The Q4 2025 earnings season delivered a clear message: supply chain digitization has crossed the threshold from competitive advantage to operational requirement. Companies that frame logistics technology as discretionary spending are falling behind those that treat it as infrastructure.

The $72 billion already committed globally is just the foundation. With projections pointing toward $147 billion by 2031, the question for logistics operators isn't whether to invest in digital capabilities — it's whether their current platform can scale with that investment.

Is your supply chain technology keeping pace with the infrastructure shift? Contact CXTMS to see how a unified TMS platform turns logistics digitization into measurable competitive advantage.