State of Commerce Operations 2026: Why 60% of Retailers Now Use AI Chatbots and What It Means for Fulfillment Logistics

Nearly nine in ten mid-market retailers reported revenue growth in 2026 — yet only a third can see their inventory clearly across channels and warehouses. That disconnect, revealed in Linnworks' newly released State of Commerce Ops 2026 report, captures the central tension shaping e-commerce fulfillment this year: growth is no longer the hard part. Scaling operations to match it is.

AI Chatbots Are Just the Tip of the Iceberg

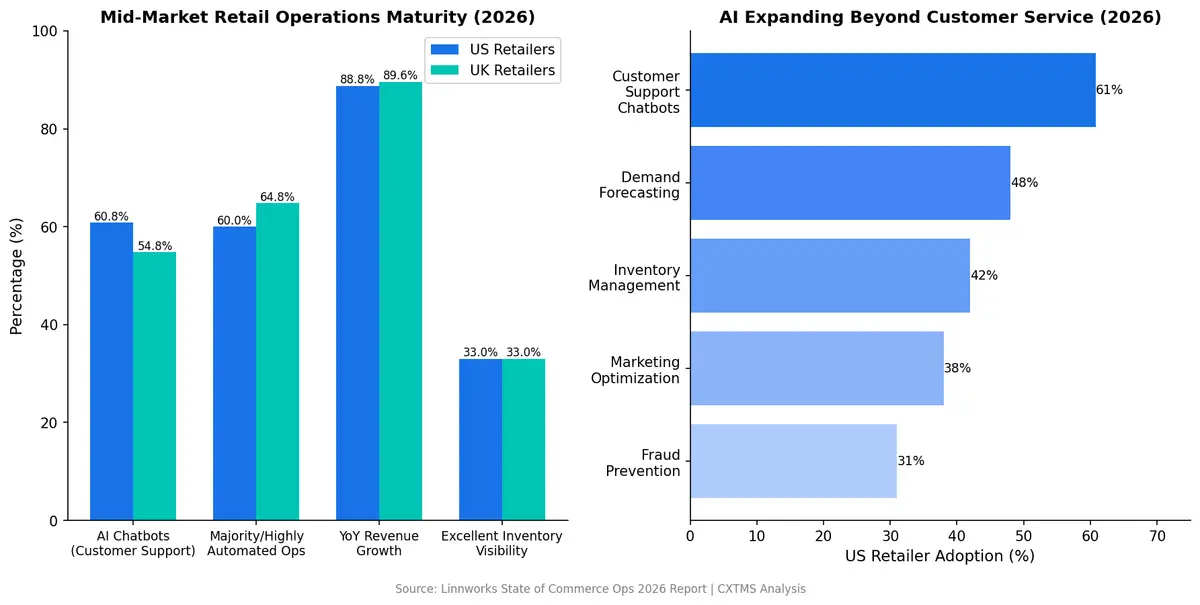

The headline number from the Linnworks survey of 500 mid-market retail leaders (businesses earning $7.5M–$100M annually) is striking: 60.8% of US retailers and 54.8% of UK retailers now use AI chatbots for customer support. But reducing this report to a chatbot adoption story misses the bigger picture.

AI is rapidly expanding beyond customer-facing conversations into operationally critical areas:

- Demand forecasting — predicting stock needs weeks before orders materialize

- Inventory and order management — automating allocation across warehouses and channels

- Marketing optimization — personalizing campaigns based on real-time purchasing signals

- Fraud prevention — flagging suspicious transactions before they ship

The pattern is clear: AI entered retail through the front door (customer service), but it's now moving into the back office where fulfillment lives.

Growth Is Everywhere — Scalability Isn't

According to the report, 89.6% of UK retailers and 88.8% of US retailers report moderate to significant year-over-year growth. That sounds like an industry firing on all cylinders. But dig deeper and the cracks appear.

Growth, the report argues, "is no longer constrained by ambition or demand — it is constrained by operational design." The retailers achieving the highest growth share a common trait: mature automation and multichannel integration. Everyone else is growing into complexity they can't manage.

The most telling statistic may be the inventory visibility gap. Only about one-third of retailers in both the US and UK report excellent inventory visibility across channels and warehouses. When you're selling on Amazon, Shopify, TikTok Shop, and your own website simultaneously, a single inventory error cascades into overselling, stockouts, cancelled orders, and negative reviews.

Automation Has Become Table Stakes

Perhaps the most sobering finding for retailers still running manual processes: automation is no longer a competitive advantage. It's a baseline requirement.

The report shows that 64.8% of UK retailers and 60.0% of US retailers operate with majority or highly automated systems. Automation adoption depth varies significantly — and those differences are increasingly reflected in growth outcomes, operational resilience, and leadership confidence.

This tracks with what McKinsey identified in their analysis of agentic commerce: fulfillment systems will need AI agents capable of automating fulfillment decisions, negotiating return logic, and orchestrating post-purchase actions. The retailers who built automated foundations in 2024–2025 are now the ones ready to deploy these agentic capabilities.

The Multichannel Fulfillment Complexity Problem

Carrier diversification emerged as a clear signal of operational maturity in the report. Retailers using multiple carriers are more resilient during peak periods, face fewer disruptions, and have more flexibility to balance cost and delivery speed.

But multichannel fulfillment creates a cascading complexity problem that most retailers underestimate:

- Order routing decisions multiply — which warehouse ships which order to minimize cost and transit time?

- Inventory synchronization must happen in near-real-time across every channel to prevent overselling

- Returns processing becomes a logistics puzzle when customers buy on one channel and return through another

- Carrier selection requires dynamic rate comparison across dozens of service levels

Without unified operations infrastructure connecting these decisions, each new sales channel adds operational drag rather than incremental revenue.

What Smart Retailers Are Doing Differently

The Linnworks data reveals a clear dividing line between retailers who are growing profitably and those drowning in operational complexity. The high performers share three characteristics:

First, they automate before they expand. Adding a new marketplace or fulfillment center before automating existing operations just multiplies chaos. Leading retailers invest in operational infrastructure first, then scale.

Second, they treat inventory as a single pool. Rather than siloing inventory by channel, mature operations maintain unified inventory views that allocate stock dynamically based on demand signals, margin targets, and fulfillment costs.

Third, they connect commerce to logistics. The gap between an order confirmation and a shipping label is where most fulfillment failures occur. Bridging that gap with integrated systems — connecting order management, warehouse operations, and carrier selection — eliminates the manual handoffs that cause delays and errors.

From Commerce Ops to Freight Execution

The Linnworks report focuses on mid-market e-commerce, but the implications extend directly into freight and transportation. As retailers automate their commerce operations, the next bottleneck shifts downstream: how do you get inventory to warehouses efficiently, and how do you ship orders to customers cost-effectively?

This is where commerce operations and transportation management converge. The same AI that optimizes order routing can inform freight consolidation decisions. The demand forecasting that prevents stockouts can also trigger proactive inbound shipment planning. The carrier diversification that builds fulfillment resilience applies equally to LTL and parcel networks.

For retailers whose commerce operations have matured to the automation baseline the report describes, the competitive frontier is now the logistics layer connecting suppliers, warehouses, and last-mile delivery.

Scaling your e-commerce fulfillment beyond the automation baseline? Contact CXTMS to see how integrated transportation management connects your commerce operations to freight execution.