Logistics Real Estate Rebalances in 2026: How Falling Vacancy Rates and Rising Rents Are Reshaping Warehouse Strategy

The U.S. logistics real estate market is entering a new chapter. After two years of rising vacancy and falling rents, the tide is turning—and shippers, 3PLs, and supply chain leaders who aren't paying attention may find themselves locked out of the best space at the worst possible time.

The Numbers Tell the Story: Vacancy Has Peaked

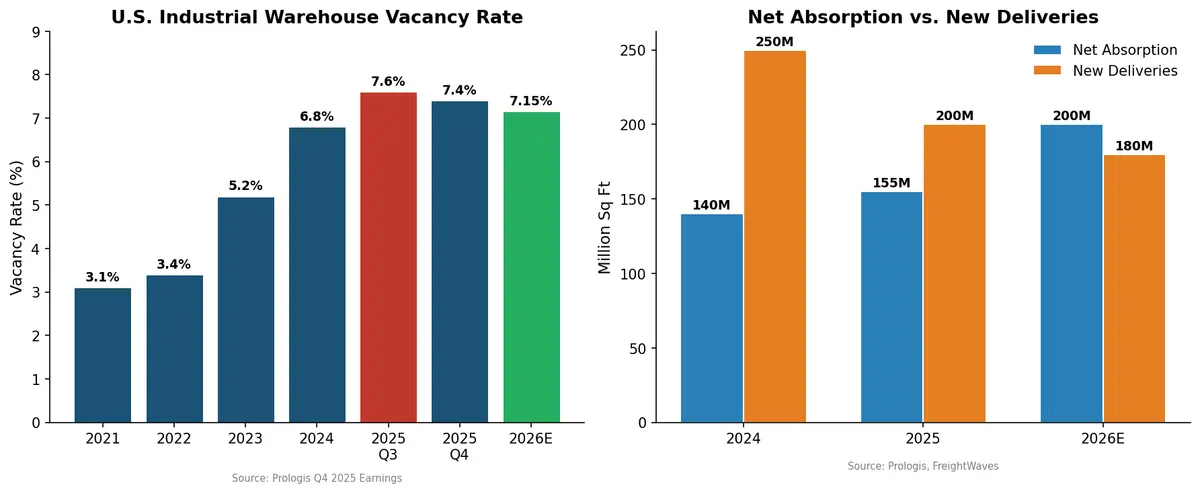

Prologis, the world's largest logistics real estate owner, reported in its Q4 2025 earnings that U.S. warehouse vacancy rates dropped to 7.4% quarter over quarter—the first meaningful decline since the post-pandemic correction began. Net absorption surged to 59 million square feet in Q4 alone, outpacing new facility completions for the first time since 2022.

That single quarter signals a structural shift. During 2023 and 2024, a wave of speculative warehouse construction flooded the market. Developers who broke ground during the e-commerce boom delivered hundreds of millions of square feet into a market where demand had cooled. Vacancy rates climbed from historic lows near 3% to over 7%.

Now the pendulum is swinging back. Prologis projects 200 million square feet of net absorption in 2026 against only 180 million square feet of new deliveries. That 20-million-square-foot gap is expected to push national vacancy down to approximately 7.1% to 7.2% by year-end, according to FreightWaves.

Rents Are Inflecting After a Painful Correction

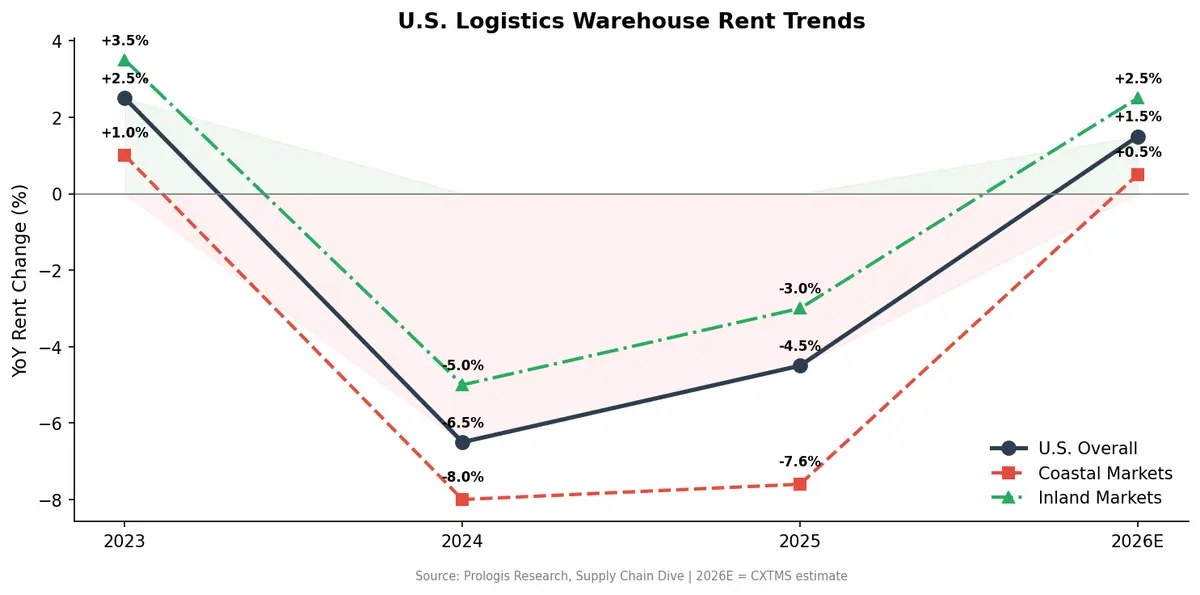

The rent story is equally compelling. U.S. logistics rents fell 4.5% year over year in 2025, following a steeper 6.5% decline in 2024, per Supply Chain Dive. Coastal markets bore the brunt with a 7.6% drop, while inland markets like Houston, Indianapolis, and Nashville posted more modest 3% declines—and in some cases actually grew.

But the correction is losing steam. Prologis CFO Tim Arndt noted on the company's Q4 earnings call that "vacancy has peaked and rents are beginning to inflect across many markets." The company's lease mark-to-market—the gap between expiring rents and current market rates—still sits at 18%, representing $800 million in future net operating income. In other words, even after two years of declines, today's market rents remain significantly above the rates locked in during pre-pandemic leases.

For tenants who signed deals during the 2023–2025 window, the pricing was favorable. For those whose leases expire in 2026 or 2027, the window of opportunity is narrowing.

E-Commerce Is Back as a Demand Driver

One of the most notable trends fueling the rebalance is the return of e-commerce as a warehouse demand driver. E-commerce represented 20% of Prologis' new leasing activity in 2025, making it the sector's best year since 2021. Large retailers are expanding distribution networks to trim delivery times and improve last-mile efficiency.

This isn't the speculative land-grab of 2021. Today's leasing is more strategic—companies are choosing locations based on transportation cost optimization and proximity to population centers rather than simply grabbing every available square foot. Prologis recorded 228 million square feet of lease signings in 2025, a record volume that reflects this renewed, data-driven approach to network expansion.

What This Means for 3PLs and Shippers

The tightening market creates a two-speed reality for logistics operators:

For 3PLs, the squeeze on available space means lease negotiations are getting harder. Operators who locked in favorable rates during the downturn are sitting on competitive advantages. Those still looking for expansion space—particularly in high-demand corridors like Southern California, the I-85 corridor, or the Dallas–Fort Worth metroplex—will face rising costs and fewer options.

For shippers, the warehouse real estate market directly impacts fulfillment costs and network agility. Key strategic considerations include:

- Lease timing: Securing multi-year commitments before rent growth accelerates

- Location optimization: Balancing cheaper inland space against transportation costs to end consumers

- Space utilization: Maximizing throughput per square foot becomes critical when space costs rise

- Flexibility: Build-to-suit versus speculative space trade-offs shift as vacancy tightens

The companies that will navigate this transition best are those with real-time visibility into their warehouse utilization, transportation costs, and network performance.

Technology as the Equalizer

When warehouse space gets expensive, efficiency becomes the competitive differentiator. Organizations that can optimize inventory placement, reduce dwell time, and coordinate inbound and outbound flows effectively will extract more value from every leased square foot.

This is where integrated TMS and WMS platforms earn their ROI. Real-time freight optimization reduces the need for buffer inventory. Dynamic routing minimizes the number of distribution points required. And data-driven network analysis helps logistics teams make informed decisions about where to expand, consolidate, or exit.

Prologis itself is betting on this trend, noting that 40% of its 2026 development starts are data centers—infrastructure that powers the AI and analytics platforms logistics companies increasingly depend on.

The Bottom Line

The 2026 logistics real estate market isn't a crisis—it's a rebalance. Vacancy is falling, rents are turning positive, and the easy deals of the past two years are disappearing. For shippers and 3PLs, the strategic imperative is clear: use data to optimize your existing footprint, lock in favorable lease terms while you still can, and invest in the technology that maximizes every square foot.

The companies that treated the downturn as a chance to build smarter networks will thrive. Those that waited will pay more for less.

Need better visibility into your warehouse and transportation network? Contact CXTMS to see how integrated logistics technology can help you stay ahead of the market.