The Intralogistics Robotics Gap: 52% Run Robots, but First-Time Buyers Are Still Stuck in Education Mode

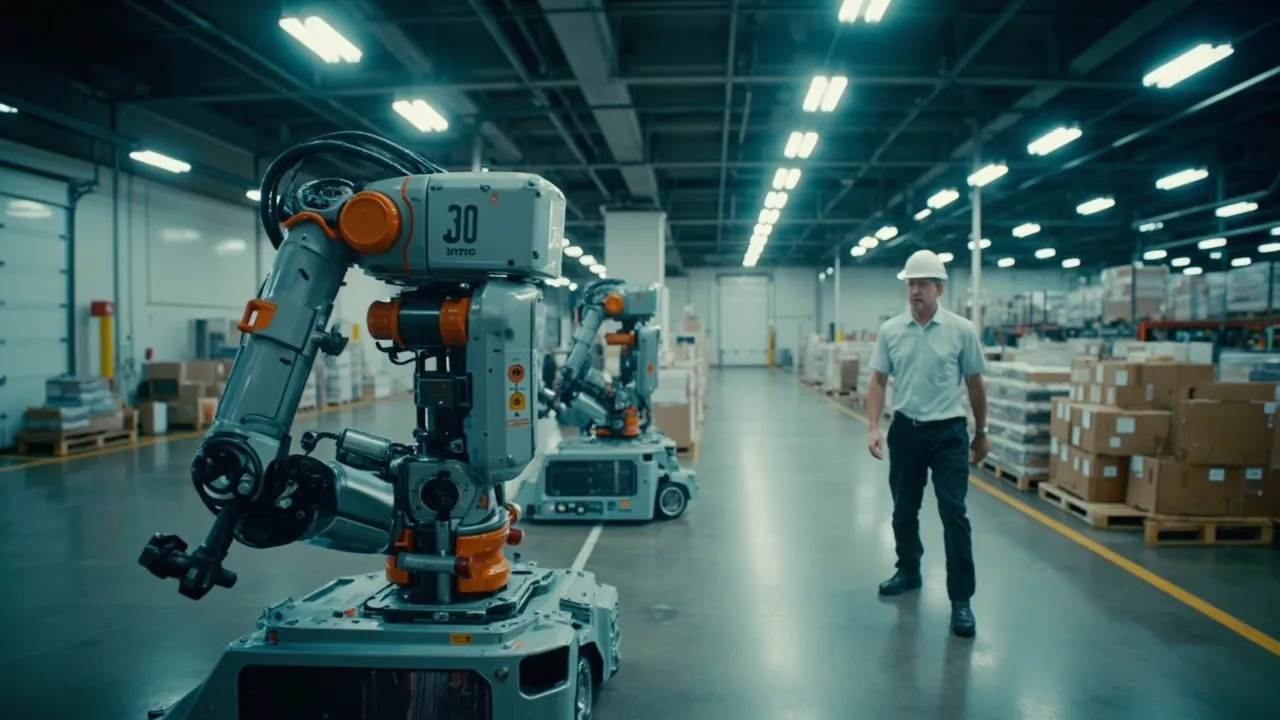

Warehouse robotics has crossed an important line: it is no longer a futuristic bet for only the largest distribution networks. It is becoming normal operating infrastructure.

But the adoption curve has a strange shape. A growing share of warehouses already run robots, and many of those deployments are meeting their goals. At the same time, a large population of first-time buyers remains stuck before the first project starts, still trying to understand vendors, ROI, integration, and operational risk.

That is the intralogistics robotics gap. The technology is maturing faster than the buyer's internal decision process.

Modern Materials Handling's 2026 Intralogistics Robotics Study, conducted by Peerless Research Group for Logistics Management, Modern Materials Handling, and Supply Chain Management Review, surveyed 166 warehouse, distribution, and manufacturing operations professionals involved in robotic automation decisions. The headline numbers are strong: 52% are already running robots, and another 32% plan to do so within three years.

Just as important, the study says 74% of deployers report hitting their business goals. That should quiet the old argument that robotics is mostly trade-show theater. In real facilities, with real constraints, robotic automation is producing results.

Yet the same report adds the caution that matters for 2026 planning: satisfaction around cost and time-to-value is more complicated, and 47% of companies still planning their first robotics initiative have not moved past the education stage.

In other words, the market is not waiting for proof that robots can work. It is waiting for better business cases.

The first project is the hardest one

Robotics vendors often sell speed, labor savings, flexibility, and scalability. Those are valid outcomes, but they are not a business case by themselves.

A warehouse leader trying to approve a first deployment has to answer more specific questions. Which process should be automated first? What labor problem is being solved: cost, availability, turnover, safety, overtime, or service consistency? How variable is order volume by day, week, and season? What happens when the robot fleet has to interact with the warehouse management system, cartonization logic, pick paths, sortation, dock schedules, and transportation cutoff times?

That is why the education-stage number matters. Nearly half of first-time planners are not simply cautious; they are missing the cross-functional operating model needed to make the first project credible.

A strong first robotics project has five ingredients: a process with measurable pain, demand variability automation can absorb, integration defined before purchase order approval, realistic time-to-value milestones, and a direct connection to transportation promises. A faster pick face does not help if orders still miss carrier cutoff, dock doors are overbooked, or parcel induction lacks accurate package data.

Robotics is moving from assistance to autonomy

The technology itself is also changing. The next wave is less about one robot helping one worker and more about autonomous systems coordinating multiple steps.

Modern Materials Handling reported that Locus Robotics launched Locus Array, a fully autonomous fulfillment system that combines mobile robotics, an integrated robotic picking arm, AI-powered perception, and autonomous execution. The system is described as a robots-to-goods model, where robots go directly to inventory and execute fulfillment tasks in the aisle rather than merely supporting a fixed manual process.

The operational idea is important even for companies that never buy that specific system. Warehouse automation is moving toward orchestration: robots, workflows, inventory movement, and demand signals coordinated in real time. That raises the upside, but it also raises the integration burden.

If autonomous systems are dynamically assigned to tasks based on demand, then bad data becomes operationally expensive. Poor slotting, inaccurate inventory, inconsistent SKU dimensions, and disconnected dock schedules can all turn a robotics investment into a faster way to create exceptions.

The lesson is blunt: robotics readiness is data readiness. Supply Chain Dive has described the same adoption curve from another angle, noting that warehouse robotics use is expanding while buyers still have to prove where automation creates measurable efficiency rather than novelty.

Fulfillment design is changing around the robot

The robotics gap also shows up in how fulfillment processes are being redesigned. Inbound Logistics recently highlighted warehouse technology that eliminates separate pick-and-pack zones and compresses work at the station. Exotec's Skypod system, for example, can process up to 600 bins an hour at each workstation and match orders with the right container at the workstation.

That points to a broader shift. Warehouse automation is not just making old processes faster. It is changing the unit of design from aisle, cart, and packing table to container, workstation, order promise, and carrier cutoff.

For e-commerce, retail replenishment, spare parts, healthcare, and time-sensitive industrial distribution, that matters. The best warehouse process is not simply the one with the highest picks per hour. It is the one that gets the right order into the right container, with accurate dimensions and documentation, early enough to hit the planned transportation mode.

That is where many robotics business cases undercount value. Labor savings may be the easiest number to present, but service reliability can be just as important. Better fulfillment flow can reduce premium freight, missed pickups, split shipments, returns from errors, and customer-service escalations.

Transportation should be in the robotics business case

Too many automation projects are evaluated inside the four walls only. That is a mistake.

A warehouse robotics investment changes transportation execution. If orders are released faster, carriers may need different appointment windows. If cartonization improves, parcel and LTL rating may change. If inventory counting becomes more frequent, allocation decisions can become more reliable. If dock staging becomes more predictable, detention and missed pickup risk should fall.

The reverse is also true. If transportation planning does not adapt, robotics value leaks out at the dock. A facility can improve pick productivity and still disappoint customers if carrier capacity, route planning, documentation, and order cutoff rules remain manual.

For freight forwarders, 3PLs, and logistics teams, this is the strategic angle. Warehouse automation should not be treated as a facility engineering project that ends at the shipping door. It should be connected to order visibility, dock schedules, shipment milestones, customer commitments, and exception management.

CXTMS is built around that connected operating layer. When transportation teams can see bookings, rates, documents, milestones, exceptions, and customer commitments in one workflow, they can turn warehouse automation gains into better delivery performance rather than isolated productivity wins.

The robotics market is no longer waiting for permission to grow. With 52% of surveyed operations already running robots and 74% of deployers hitting their goals, the proof is there. The remaining challenge is practical: help first-time buyers move from education to execution with a business case that includes labor, throughput, integration, and transportation impact.

If your team is evaluating warehouse robotics and needs transportation execution to keep pace with fulfillment automation, schedule a CXTMS demo.